The Returns You Keep

The advice to “stay invested” is easy to give. It’s also suspiciously convenient when it comes from a fund manager who benefits when you don’t leave.

So we tested it. Eighteen Flexi Cap funds. Over a decade of data. A simulated investor who exits when their fund underperforms.

The answer is uncomfortable for different reasons than we anticipated.

Investor returns depend on two decisions. Which fund you pick. And what you do after you pick. Research suggests most investors get at least one wrong. The DALBAR Quantitative Analysis of Investor Behaviour estimates investors trail the very funds they invest in by nearly 2% annually. Morningstar’s Mind the Gap 2025 report found a 1% gap over a decade.

We wanted to see how this holds for Indian Equity Funds. So we analysed 18 flexi cap funds with at least a decade of history, examining both the range of outcomes across funds and what happens when investors react to underperformance by switching.

The findings: fund choice creates enormous variance in outcomes, but after accounting for taxes, reacting to that variance almost never helps.

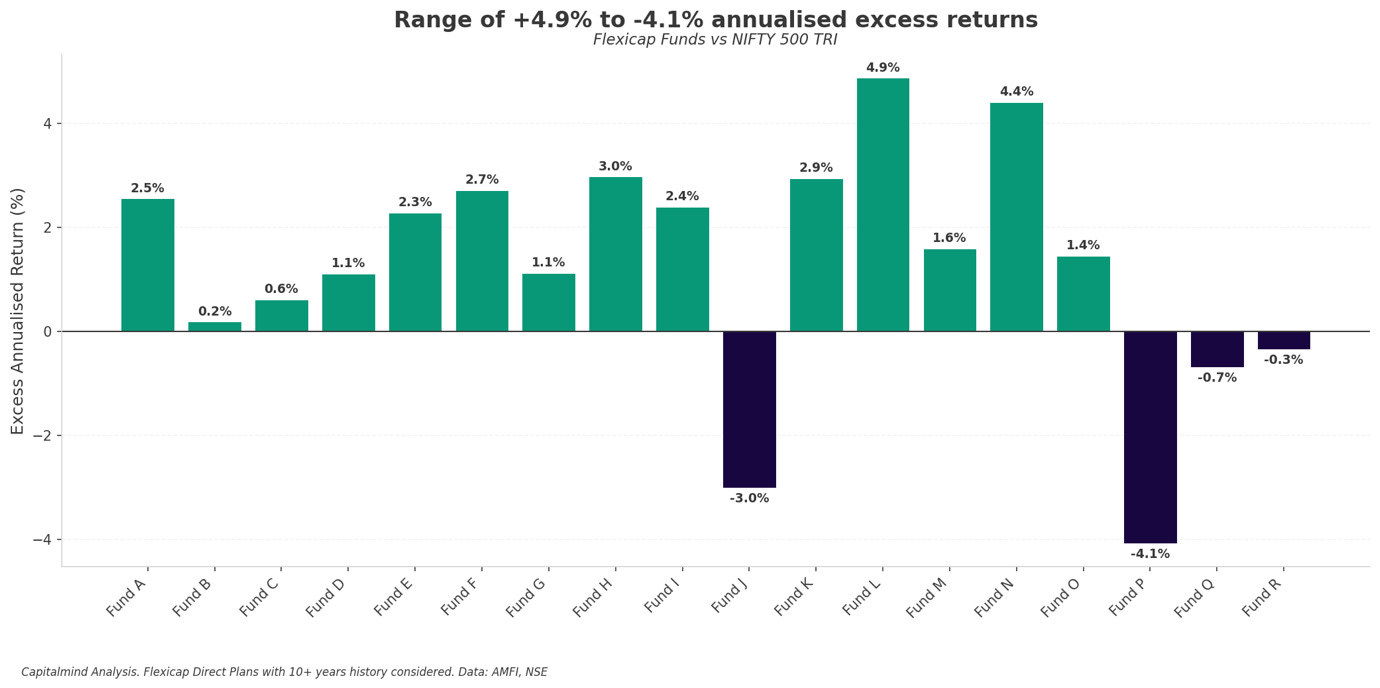

9% apart: What fund choice costs

First, one obvious and one not-so-obvious insight from the data.

The best-performer in our data set delivered nearly 5% alpha i.e. excess return over the benchmark. The worst performer trailed by 4%.

A 9% difference in annual return compounded over more than a decade. That translates to a 3x difference in terminal wealth on the same starting investment.

The obvious truth, picking the right fund clearly matters.

Chart shows the 18 funds’ annualised excess returns over the Nifty 500.

Of the 18 Flexi cap funds with 10+ year track records, 14 beat the benchmark over the full period. Only four did not.

Picking the right fund has been more about avoiding the consistent laggards and not about finding that one superstar.

Unless the task you set yourself is to identify the absolute top-performer, which is harder than it looks without the benefit of hindsight.

The price of admission

A finding that applies, regardless of fund quality: periodic underperformance is the norm, not the exception.

We calculated, what percentage of rolling 1-year periods, each fund trailed the benchmark.

The best-performing fund in terms of excess returns, Fund L, spent a quarter of the period underperforming the benchmark. That means an investor tracking its performance would cringe once in every four periods.

Other solid performers, Fund N, F, H, I; spent a third of their time trailing the benchmark.

At the other end, the worst performers spent 70 to nearly 80% of their time underperforming. But even the outperforming funds on average underperformed (on one-year basis), 40% of the time.

Fund O trailed the benchmark half the time yet outperformed overall. Comparatively, Fund R trailed less often, yet underperformed. Frequency of underperformance didn’t predict outcome.

Good fund or Bad fund, underperformance ranging from a quarter to half the time is inevitable. The experience of holding an active fund includes long stretches where it feels like a mistake.

What switching actually costs

Underperformance might be universal, but it’s still hard to stomach. Especially when the fund you’re in trails the index while your friend mentions her fund outperforming that same index by a distance.

What does acting on that instinct actually cost?

We simulated a reactive investor, one who exits when a fund’s rolling 1-year return trails the benchmark by more than 5%, and re-enters when it leads by more than 5%. During exit periods, we assume that instead of sitting in cash, they invest in the index, thus staying fully in equities.

Notice how this is a generous assumption. Real investors who exit a fund on account of its underperformance rarely park rationally in the index. They are more prone to chasing the next “hot” fund. Our reactive investor is more disciplined than most.

The pre-tax picture looks like a coin flip. Before accounting for taxes, the reactive investors beat buying-and-holding in 9 funds, lost in 8, and tied in 1. You could look at this and conclude: “Reactive selling is 50-50, so it’s not bad.”

But taxes change everything. If we assume each exit triggers a 12.5% long-term capital gains tax on accumulated gains, the picture changes dramatically.

After tax, the buy-and-hold investor does better than the reactive investor in 17 of 18 funds.

The single exception was Fund P, the worst performer in the dataset, trailing the benchmark by 4% annually. Here, the reactive investor still trailed the index, but by a much smaller margin by exiting and re-entering than if they had held on to the laggard.

The table below shows the comparison of the Buy-and-Hold and the Reactive Investor, with and without tax impact. Pre-tax results sort of justify reactive behaviour, post-tax reality undermines it.

The data tells us three things. The gap between best and worst was large, which means fund selection deserves more attention than it typically gets. Even excellent funds underperform frequently, which means holding requires preparation, not just conviction. And reactive switching destroyed value in almost every case, which means the bar for action should be high.

What the data does not tell us is how to pick Fund L over Fund P in advance, or how to hold Fund L through the quarters it trailed. It does, however, narrow the problem. We’re not looking for a needle in a haystack, 14 of 18 funds beat the benchmark. We’re trying to avoid the four that didn’t, and then stay put long enough to capture the gains. Here’s what we think that requires.

Picking well

If fund selection matters this much, how do you make the decision, other than in hindsight?

What returns don’t tell you

Returns tell you what happened. They don’t reveal whether they are repeatable.

Look instead for signals of durable process: Does the fund communicate clearly what it owns and why? Does it acknowledge when things aren’t working? Is there consistency between stated approach and actual holdings? Would removing a key person fundamentally change how the fund invests?

Most of the top performers in the 18-fund sample exhibited these characteristics. We can’t prove causation from an 18-fund sample, and qualitative assessment resists backtesting. But the pattern was there.

Buy the fund you can hold

Before investing, understand what the fund is trying to do. What’s the investment approach? What market environments will favour it? What conditions will make it struggle?

And most importantly, do you agree with how the fund views markets?

Let’s say you believe that returns get made from investing in low multiple stocks with decent earnings yield. However, you bought a fund because it topped last year’s returns or because someone recommended it strongly. It turns out this fund invests in high-growth companies because that is its view of the markets. Then you’ve set yourself a hard challenge by picking a fund that has a completely different view from your own.

The first bad stretch that fund goes through will feel like a mistake. If you bought it because you understood and believed in the approach, the same bad stretch will feel like turbulence, to be ridden out unperturbed.

A momentum fund will struggle when trends reverse. A value fund will lag when growth dominates. A concentrated portfolio will be more volatile than a diversified one. Think of them as features. If you don’t understand or agree with them going in, you’ll interpret them as failures and leave at the wrong time.

Be ok to sin, a little

Markets are complex adaptive systems. When a strategy works, capital flows toward it. As more capital chases the same edge, the edge dulls. The landscape shifts in response to what participants do, which means the conditions that made a strategy successful often erode precisely because it was successful.

Evolutionary biologists call this the Red Queen effect: you have to keep running just to stay in place. In markets, strategies that don’t evolve get arbitraged away or simply stop working as the environment changes around them.

The uncomfortable implication: investment beliefs that served you well may not survive the next decade. Value investing dominated for generations, then spent years looking obsolete. Momentum works until regime changes punish it severely. Small-cap premiums appear and vanish across eras and geographies. No approach carries a permanent edge.

This doesn’t mean abandoning conviction. But it suggests holding conviction with humility. If your entire portfolio reflects a single view of how markets work, you’re betting that view remains valid indefinitely.

A partial allocation to a fund whose philosophy differs from yours acknowledges you might be wrong, or that markets might evolve in ways that favour a different approach.

Start small. Observe how it behaves through different conditions. Notice how you feel holding it.

The goal is making decisions you can live with, not predicting which worldview markets will reward next.

Holding well

The data shows that even having picked well means underperforming a third to almost half the time. The question is what you do next.

Style drought or process failure?

Ask: Is this a bad time for the fund’s style, or is the fund’s process broken?

A value-oriented fund trailing in a momentum-driven market is the former. The style is out of favour; the process may be intact. This is when patience is appropriate, and often when it’s hardest. A fund drifting from its stated mandate, or one with a mandate too vague to evaluate, is the latter.

The cost is certain, the benefit isn’t

The fund you switch to must compensate for the certain costs of exiting your current one. Those costs are known. Whether the new fund delivers is not.

The disposition effect works against us here: we’re prone to holding losers too long and selling winners too early. The goal isn’t to never sell. It’s to sell for the right reasons, knowing what it costs.

Our side, your side

The behaviour gap is real. We saw it in 17 of 18 Funds over the past decade. But the lesson isn’t simply to “stay invested”. That’s too convenient coming from a fund manager who benefits when you don’t leave.

The honest version is messier:

Investor returns depend on two decisions, both of them not straightforward. Picking a fund worth holding. And then actually holding it when doing so feels foolish.

The investors who do well get both right, or at least avoid getting both catastrophically wrong. They choose funds based on process, not recent glory. They expect discomfort and don’t mistake it for a signal. They don’t go all-in, and take advantage of the ability to partially allocate before scaling up. And when they decide to move, they do it deliberately, not reactively.

Our goal at Capitalmind is to build funds worth staying in. Our investment philosophy is our own, shaped by what we’ve learned, tested, and found to work for us. We’re not claiming it’s the only way, just that it’s ours, not inherited, not imitated. And to be transparent about what we do. Honest when we’re struggling. Consistent in our approach, with a bias towards gradual sustained improvement.

We’ll have difficult stretches, that’s a given. When that happens, we’ll tell you what we’re seeing, whether we think it’s cyclical or structural, and what we’re doing about it. That’s our side of the deal.

Your side is knowing that at least a quarter to a third of your holding period will probably feel uncomfortable.

The returns your fund earns are only half the story. The returns you keep depend on you.

This analysis has blind spots. If you see them, or if your experience contradicts what we found, let me know.

Anoop Vijaykumar @CalmInvestor · anoop.vijaykumar@capitalmindmf.com

References in this article:

DALBAR’s Quantitative Analysis of Investor Behavior (QAIB) link

Morningstar’s “Mind the Gap” 2025 Report link

The Disposition to Sell Winners too Early and Ride Losers too Long (Hersh Shefrin and Meir Statman) link