Forget Stocks for a bit. Get your Asset Allocation right

Did you know a 50:50 NIFTY + FD portfolio beats the NIFTY over 30 years?

This article was first published on capitalmind.in

You've heard of the three C's by now. Courage. Cash. Conviction. You're probably sick of them already.

For the uninitiated, the three C's are meant to galvanize the timid investor trying hard to avert her gaze from a screen dripping red.

Don't you know, they say, if your horizon is longterm, you can't go wrong with equities?

Equities outperform everything else out there. But great victory demands great sacrifice. So build Conviction, be Courageous, and deploy that Cash! Three C's.

But where's the cash? You wonder to yourself. Weren't the same C's called on to invest when markets had just made a new high? You clearly remember the argument at that time. Price doesn't matter if you hold quality businesses for the long term. Now sounds like something a seller would say.

But you look through your holdings anyway. There's that little bit of cash leftover from finally selling that stock you held since the 2008 crash. What's the IRR on an 80% loss spanning 12 years, you wonder. Then there's that pittance of a dividend from your current portfolio. At least the dividend yield has perked up since prices halved in two months. So much for Growth at a Reasonable Price.

At least you have something. You look at the screen. Eyes, flitting from one deep red occupant to another. Buy more of existing stocks that have lost so much?

Or start afresh? Those defensive stocks that were always ridiculously priced have dropped only half as much as the rest of the market. In fact, they're moving up even as you watch. Up nearly 2% for the day!

It makes sense that they would be the first to recover (Conviction. You say to yourself). You buy.

A month later they're indistinguishable on your holdings screen from the rest. A sea of red.

You curse (under you breath). Goddamn chickens*** investing catchphrases.

The problem really is our need to seek out stories that appeal to our limbic system, "emotional brain" as its called.

For instance, the one about the inherent God-given superiority of equities over more secure financial instruments for long-term performance.

After all, How can part ownership in a thriving business with all the inherent uncertainty not be far more rewarding than a modest yet fixed rent for your money?

Put another way, the theory and popular perception says...

Over a long enough time frame, Equity gives (significantly) higher return than Debt. Ergo, Debt is for folks nearing retirement and/or cannot afford to invest for the "long term" while Equity is the rocky but certain path to financial independence.

Equities beat Fixed Deposits. Duh.

Here's proof.

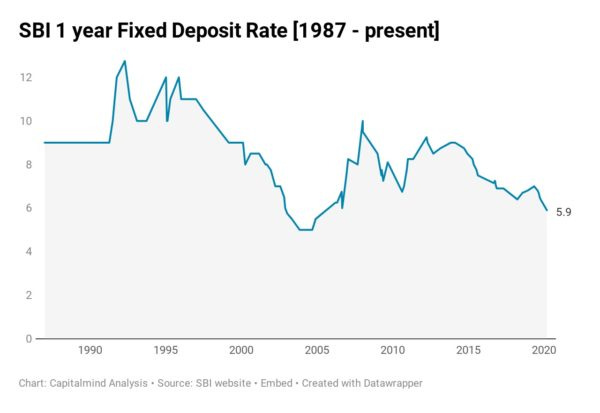

Chart shows SBI 1 year Fixed Deposit Rates from 1987, currently at 5.9%

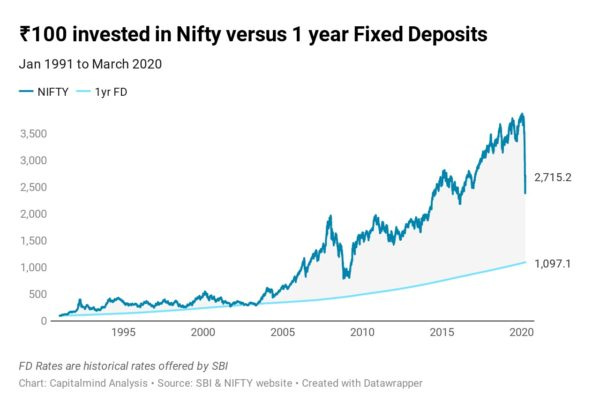

Chart shows the comparison between putting ₹100 into a 1 year FD and rolling it over for the next 29 years versus buying and holding the NIFTY starting Jan 1991.

By putting the money into the NIFTY, you end up with 2.5x the value you would have by putting that money into 1-year Term Deposits for 29 years, from 1992 to 2020. That number was an even more convincing 3.6x just a few weeks ago, as of Jan 14th, but still comprehensive. Note we ignored taxes on the FD interest because there are ways to set that off against costs like business expenses.

So far so good.

But...

Consider these two points:

The NIFTY investment suffers drawdowns as much as 60% (Oct 2008) from its previous peak. The FD investment never closes below its previous value.

Nine years from the start of our little thought experiment, on 20th Sep 2001, the NIFTY investment dips below the value of the Fixed Deposit investment, albeit briefly